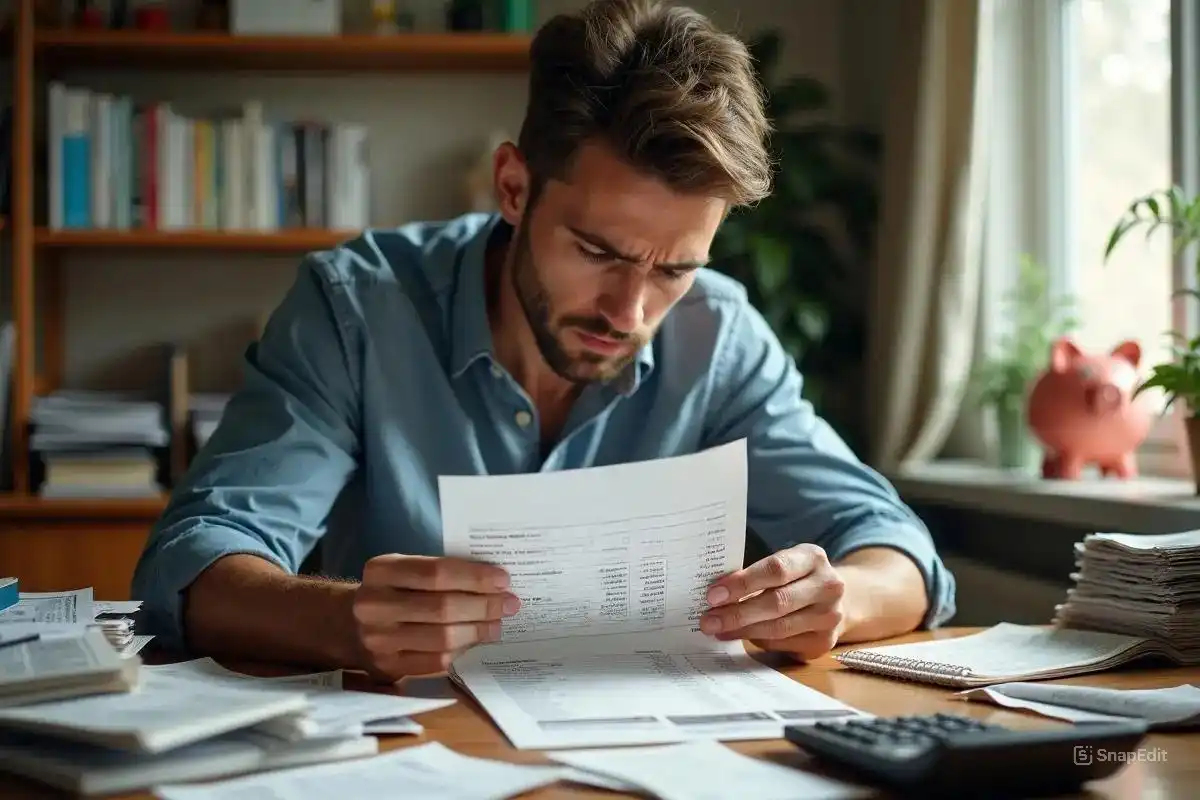

When you have an emergency fund, it feels great. That spare cash that everyone suggests you have just in case, that safety net that’s supposed to save you from a world of despair when the unexpected bad happens to you. What people don’t take into consideration, though, is when the bad happens and it’s worse than what’s in your savings. But what happens when your $2,000 emergency fund isn’t enough to support a $5,000 need?

This is not an uncommon situation; more people than they care to admit fall victim to it. Emergency funds are built little by little over time. One paycheck at a time. But the thing is, when emergencies happen, they don’t take stock of how much someone has saved. A medical emergency doesn’t care how much is sitting in the bank when it happens. A car accident doesn’t see a $2,500 repair and know that you’re halfway to saving that much; it only sees the bill.

It’s the inequity that makes stress levels insane, and when forced to make difficult decisions, it’s even more infuriating. People are naturally going to panic; they’re naturally going to feel bad for themselves for not saving much more but none of that helps in the moment. Instead, it’s important to realize the inequity and act as appropriately as possible to fill the gap without putting people into ruin for the long-term.

Contents

Assessing The Real Gap

Before assessing where people fall short, it’s important first to establish what’s needed and what’s available. This shouldn’t be too scary an assessment out of fear that it’ll cost worse than it is but factual assessments are critical.

Get estimates where applicable; if someone can give a ballpark, mechanic, medical professional, attempt to decipher what’s mandatory versus suggested so the costs don’t inflate. Sometimes what seems like a catastrophic issue turns out to be a minor one once the cost is obtained.

Then assess what’s truly available to combat the total emergency. An emergency fund is one thing, but any cash on hand? Is there access to other income soon? Can things be sold in time without drastic life changes? Too many people forget their plight in the moment because they’re too engulfed in the panic over the emergency.

For example, if it’s determined there’s a $2,000 gap and all that’s available at the moment is $2,000 in cash in an emergency fund, no problem, but if it’s determined there’s a $5,000 gap and all they have in their emergency fund is $2,000, now that’s bad. But not as bad as previously anticipated over a problem. The less cash someone needs immediately makes them feel better.

Short Term Solutions: Borrowing

Regardless of anything else at this time, if someone’s cash isn’t cutting it, borrowing is inevitably going to be part of life with no question if it has to happen, it’s only a matter of how it can be secured without making things worse down the line.

Two options

There are two options, to borrow or not, and all will come at a cost due to financial negligence or high interest rates. The first option is credit cards, which can help pay for smaller expenditures, but only limited if credit remains available for charged use, immediate access without waiting for approval can be appealing, but sky high interest is troubling if paid back too late, or not at all (which devastates credit as well). For smaller dollar amounts (a few hundreds), this might be an accessible option if repayment can happen with a paycheck or two down the line of overtime from extra pay.

The second option, emergency loans exist through certain establishments just for these crazy surprises and have faster access than traditional loans for smaller amounts than personal loans might typically give. For bigger amounts in relatively quicker situations, lines of credit are available, but these must have been established ahead of time, this option, like a credit card, just for emergencies, means access isn’t always guaranteed unless prearranged, with most people not thinking they’re going to need it down the line.

Loans through traditional banks or credit unions also take time but offer better interest rates for those with established relationships with those banks.

The kicker with this option is there’s always a catch that can wildly fluctuate depending on person accessibility or stipulations given interest rates low one day and sky-high the next; fees will also accumulate so quicker options can cost more, and urgency gives some people leverage over others without making them ever use something else until then that might not have access faster.

Payment Plans and Negotiation

Not everyone should pay right away, but with a big gap created between what was wanted and what was feasible, many professionals/service providers will offer help in this situation, as long as they’re established companies offering services paid after. But too many people fail to take advantage of this option because it calls vulnerability into question ultimately asking why they can’t pay immediately up front.

Medical services typically come with payment options (doctors don’t want to stop receiving payment); repairs might yield staggered prices over a month or two; looking for breaks on price or time to pay straight up with almost unavoidable circumstances work, they want good reviews, too! In fact, getting honest with those needs is key instead of assuming everyone wants everything immediately all at once, and they’ll never work with them again when that’s simply not true (they’re worse off saying “no” anyway).

Use your emergency fund for any additional cash on hand and give yourself some dignity, and see how much you can pay and when afterward, because after fluffing up an emergency fund beforehand, isn’t too horrible of an appeal for sympathy, or final project equity rendered after the service if applicable.

Multiple Solutions Instead of One Big Solution

Sometimes emergencies (especially one based on costs) don’t lend themselves into one big solution, instead, smaller solutions are better over time. Use part of your emergency fund, charge part on your credit card, ask for help with payment plans, sell what you have, make up the difference working some overtime while working payments out for that amount instead.

There’s no reason to completely blow up everything in one shot, all at once; this devastates the entire process across the board with holistic efforts gone too far. Instead, multiple efforts fill pieces sooner than later, and a staggered decrease instead of hitting them all at once, they can use overlap enough this way to maintain savings down the road (most people think they only get one big assessed amount but they can find it over time elsewhere too!).

This takes more organization but it provides better success with payment due since amounts and timing requested become more responsible now than all at once, and gaps assessed after retroactively could’ve been granted down the line anyway, although ultimately assessed retroactively based on cumulative amounts up front that should’ve been assessed before anything happened anyway!

What Not To Do!

If anything exacerbates an already expansive hole, it’s denying better options exist in the name of temporary solutions that explode into trouble later instead of simple solutions learned through experience, not mishandled presumed timelines, and costs beat nothing worse ever!

Payday loans take that immediate accessibility into immediate account; loaning more hoops through which people must jump set them back worse with interest rates few can recover from either, not paying their initial month’s loan into hoops anyway means those caught in them can’t use their money elsewhere viable before getting themselves into debt.

Cash advances against 401k loans seem like a possibility, but tax ramifications down the line exist after penalties shove them back down your throat; bothering their circumstances compounded exponentially, like something made up that was never supposed to happen.

For extra expenses due on existing incurred necessities, the double-whammy will only rear its ugly head down the line, and if they come back. “Just this once!” turns into habitual “I’ll deal with it later” situations never materialized especially when later comes 10-fold down the line, and sympathy given extenuating circumstances where appropriate will only screw them over because they resent the extenuating circumstances for expediency where it should’ve worked out this way!

Anything needing expedited planning should be worth it since they’re less effective without hindsight dealing with what history told them! Another mistake is borrowing too little out of fear, but if someone only earmarks $2,000 for emergencies but needs $3,000, they should suck it up and realize they need $3,000! If someone only needs another $2,000 after gap assessments but only finds $2,000 extra, they better bring that discrepancy to attention pronto, they won’t have access once neediness happens!

Don’t fear half-measures from the start, or they’ll explode catastrophically later!

What’s Next?

Once everything equates idealistic projections deflate; real life concerns enter about how people get back on track from unfortunate prescience going forward? Emergency funds need refilling, whether or not they’ve surpassed threshold levels, but idealized whatever level they are threshold levels compared to anyone suggesting them who’ve never found themselves with these issues before (unfortunately) but anything’s better than nothing! Ideally people can get right back to where they were before this happened but realistically speaking, with no certain hiring and directed discretionary dollars ignored against phenomenal gaps, they need to acknowledge those emotional and financial setbacks.

Building Back Stronger

The path forward after an emergency that depletes savings isn’t just about replacing what was lost. It’s about learning from the experience and building better systems for next time. Start by focusing on immediate recovery, repaying any borrowed funds as quickly as reasonable without sacrificing basic needs. Set small, achievable milestones for rebuilding the emergency fund rather than trying to replace everything at once.

Consider what the emergency revealed about financial preparedness. Was the initial emergency fund target realistic? Should there be separate savings categories for different types of emergencies? Medical expenses, car repairs, and home maintenance might deserve their own dedicated funds rather than pulling from one general emergency account.

The goal is reaching a point where the next unexpected expense, and there will be a next one, doesn’t feel quite so devastating. Where the gap between savings and reality becomes smaller each time. Where the panic lessens because systems are in place to handle what life throws your way. That’s financial resilience, not perfection, just better preparation and smarter responses each time around.